2025 Country Update

{kind=link}

National PV Policy Programme

With over 40% of free-standing homes powered by solar, and an estimated 1.6 kW per capita installed PV, policy is now framed around dispatchable capacity.

A major policy in the federal Cheaper Home Batteries Program was launched on 1 July 2025, providing a 30% rebate on battery installations and driving record-breaking uptake, with the installation of over 165,000 household batteries to year end, with an average size of over 20 kWhr. This followed an expansion, in 2023 of the Capacity Investment Scheme targeting 32 GW of new capacity nationally, made up of 23 GW of renewable capacity and 9 GW of clean dispatchable capacity by 2027.

Large scale solar investments (over 100 kWp) receive tradeable certificates for energy generated, while small -scale systems (less than 100 kWp) are supported through a Small -Scale Renewable Energy Scheme (SRES) based on an assessment of the amount of generation they are deemed to produce until the end of 2030. Small systems receive an up-front capital cost reduction through this process, with the level of support decreasing every year to 2030.

The Large-Scale Renewable Energy Target (LRET) of 33,000 GWh of renewable electricity annually saw the installation of close to 9 GW of solar installations. The larger challenge for utility scale solar now is curtailment due to excess solar. As a result, utility‑scale solar in 2025 faced investment challenges as well as ongoing delays, while distributed rooftop systems and home batteries outperformed expectations. Recent policy adjustments reflect a shift to support for large- and small-scale storage.

2025 saw the release of funds under the Australian government commitment of $1 billion to an initiative aimed at building Australian solar PV manufacturing capability and supply chain resilience, informed by a 2024 analysis of the solar supply chain (APVI, Silicon to Solar).

National programmes in support of solar PV are also complemented by State based schemes, that seek to attract new investment in clean energy projects. Examples include Renewable Energy Zones (REZs) that aim to combine utility scale solar with wind, storage and high-voltage transmission to deliver energy to load centres. By co-ordinating investment, connection and location with respect to load, multiple generators and storage, the REZ can capitalise on economies of scale to deliver cheap, reliable and clean electricity.

Research, Development and Demonstration

PV research, development and demonstration are supported at the National, as well as the State and Territory level. In 2025, research was supported by the Australian Renewable Energy Agency (ARENA), the Australian Research Council and Co-Operative Research Centres.

The Australian Centre for Advanced Photovoltaics (ACAP) was established in 2013 to coordinate solar PV research nationally. ACAP is a national centre, hosted at UNSW, with Professor Martin Green as Founding Director. Funded by ARENA, ACAP has partners at leading research institutions around Australia including ANU, CSIRO, the Universities of Melbourne, Sydney and Queensland and Monash Uni. After ten successful years, ACAP funding was extended in 2023 supported by $45m AUD from ARENA and $10m AUD from partners.

ARENA also funded a host of new initiatives targeting commercialisation of research outcomes, making close to $60m AUD available over five years from 2023 and a further $80m AUD available in late 2025, under an Ultra Low-Cost Solar program, aiming to drive the levelized cost of electricity from large-scale solar down from the current $50/MWhr to below $20/MWhr. In addition, the federal government, under its education ministry, supported an initiative in research acceleration in the area of Recycling and Clean Energy (TRACE) with a program stream on solar technologies. The program has an ambitious goal to move rapidly to establish an innovation ecosystem to get research solutions to market faster.

Australia is active in all IEA PVPS tasks. Australia’s participation in the IEA PVPS program is supported by the Department of Climate Change, Energy, Environment and Water (DCCEEW).

Industry and Market Development

Australia saw an estimated 4.9 GW of solar installed in total in 2025, with over 2.7 GW of rooftop solar and over 2.2 GW of utility scale solar. This number may increase once all new installations are reported for the year. If so, the market will remain stable at the historical 5-year average of 4.8 GW/year.

Total installed solar capacity is now around 45 GW, 30 GW of which is rooftop solar. Solar costs stabilized in 2024-2025, with the average price per watt (installed system prices, with incentives) at $0.90.

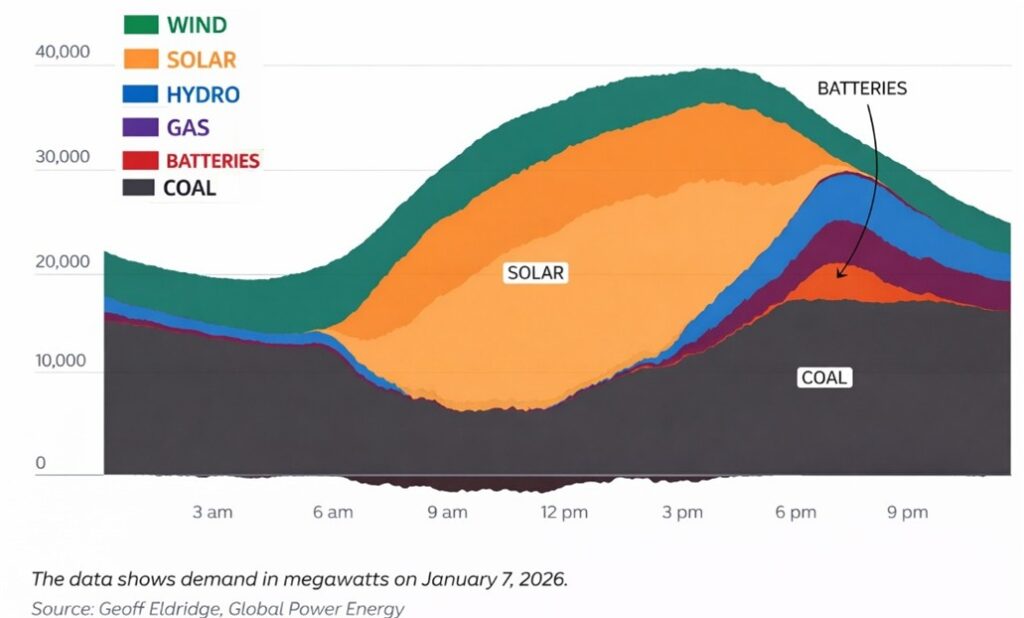

Rooftop solar claimed an annual average fraction of total electricity demand of around 15%, while large-scale solar projects contributed over 7%, for an estimate of 22% of total electricity needs being met by solar over 2025. In Q4-2025, Australia’s main grid reached a record renewable (wind and solar) share of more than 50 per cent as demand for power reached a record high and while electricity prices fell to their lowest value in two years (ABC News).

The Australian storage market remained strong in 2025, with the Clean Energy Regulator now tracking and reporting battery installations. A new federal government initiative to support household battery installs saw over 165,000 batteries installed in the 6 months to the end of the year, more than the sum total of ten years prior in voluntary reporting, resulting in 4.3 GWhr of storage capacity added.

The Australian market remains favorably viewed by overseas solar, battery and inverter manufacturers due to its high electricity prices, low feed-in tariffs, excellent solar resource, and large uptake of residential PV. There are also a large number of large-scale battery deployments planned, as excess solar in the middle of the day results in curtailment, and evening peaks challenge grid capacity.

2026 is expected to see stability in residential rooftop solar and continued growth in commercial and industrial installations. The economic fundamentals for residential and commercial PV are outstanding. Australia’s high electricity prices and inexpensive PV systems means payback can commonly be achieved in 3-5 years; a situation that looks set to continue in 2026. Larger scale behind the meter PV and battery systems are increasingly attractive for the industrial and mining sectors.

Renewed investment in large scale solar and batteries is expected to start to yield projects and connections in 2026, with a pipeline of projects aimed at 23 GW of renewable capacity and 9 GW of clean dispatchable capacity to be delivered before 2027.

Participants from Australia

University of Melbourne

Rebecca YANG

Task - 1

Task - 12

University of New South Wales (UNSW)

MOONYONG Kim

Rong DENG

Yansong SHEN

Task - 13

RINA Consulting

Carlos David RODRÍGUEZ-GALLEGOS

University of New South Wales (UNSW)

Bram HOEX

Ziv HAMERI

Task - 15

University of Melbourne

Rebecca YANG

Yusen ZHAO

Task - 16

University of New South Wales (UNSW)

KAY Merlinde

University of South Australia (UniSA)

John BOLAND

Task - 17

IT Power Australia

MCDONALD Julia

University of New South Wales (UNSW)

EKINS-DAUKES NJ

Task - 18

Ekistica

RODDEN Paul

Global Sustainable Energy Solutions (GSES)

MARTELL Christopher

STAPLETON Geoff

Task - 20

University of Adelaide