2025 Country Update

National PV Policy

The French National PV policy is built around a series of support mechanisms including Call-for-Tenders for the larger installations and Feed-in Tariffs for the smaller ones.

As module prices dropped and new capacity increased, the mechanisms for reducing tariffs as a factor of increased capacity were adjusted, resulting in increasing target volumes but decreasing tariff values. All of these measures are aimed at supporting the photovoltaic sector in achieving the objectives assigned to it in the 10-year Energy Programme Decree (PPE), the main French strategic document that sets the development trajectories for the various renewable energy sectors.

In February 2026, the new PPE Decree was published, with a delay of more than two years. For the solar sector, the new action plan sets targets of 48 GWAC of installed capacity by 2030 and between 55 GWAC and 80 GWAC by 2035. This trajectory corresponds to an average annual increase in capacity of approximately 3.5 GWAC (4.3 GWDC), a

significantly slower growth rate than that observed in recent years (6.1 GWDC in 2024 and 7.6 GWDC in 2025). In terms of electricity production, the new PPE sets a target of approximately 59 TWh by 2030 and approximately 67 to 98 TWh by 2035. According to these objectives, the photovoltaic sector is foreseen to become the first renewable energy for electricity generation in France, ahead of onshore or offshore wind power and hydro power. This national plan will need to be adapted by each of the French regions, which will have to set their own capacity and power targets for 2030 and 2035. The regions will then be able to make use of the previously defined renewable energy acceleration zones. These zones define, for each renewable energy sector, areas identified as suitable for future projects. In these areas, simplified procedures will be implemented to reduce administrative lead times.

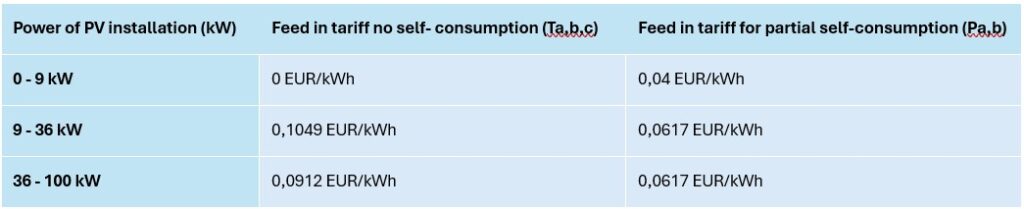

Concerning the residential installations or solar plants on buildings, barns, and parking canopies, with a capacity from 100 kWp to a maximum of 500 kWp, the support mechanisms changed in 2025. The revision of the S21 scheme in March 2025 reviewed eligibility criteria, reduced subsidies, and partially shifted the scheme towards a competitive allocation system. The former Feed-in Tariff support was turned into a simplified Call-for-Tenders system. The first one was held in September 2025, but a significantly lower capacity was allocated as compared to the initially intended one (see table 1). The reform also introduced stricter requirements for projects, including a financial guarantee of €10 000 for each complete connection application for installations over 100 kWp.

Changes have also impacted the residential installations up to 9 kWp, where the option to sell the whole electricity production to the grid is not allowed anymore. Now, only the injection of surplus electricity into the grid is possible, but with a very low Feed-in Tariff per kWh (see table 2). However, since October 2025, private persons can benefit, under specific conditions, from a reduced VAT rate of 5.5% on the purchase of panels for residential installations. The main condition concerns the carbon footprint of the modules, which must be less than 530 kgCO₂ eq/kWp.

Research, Development and Demonstration

Research and development (R&D) in the photovoltaic sector in France is based on a structured framework that integrates public and private research, technological innovation, and industrial development. Every stage of the value chain is covered, from basic materials research to production.

Among the public sector players, the two major organisations are the French Alternative Energies and Atomic Energy Commission (CEA) and the National Centre for Scientific Research (CNRS). In the field of PV, they are active in semiconductor physics, materials chemistry, and energy engineering. These two organisations also lead (or co-lead) several networks of R&D stakeholders, some of which focus on photovoltaic energy, such as CEA-Liten or the Lyon Institute of Nanotechnologies (INL). Furthermore, the CEA and the CNRS are founding members of the National Alliance for the Coordination of Energy Research (ANCRE), which plays a strategic role in defining major scientific orientations and research priorities, coordinating stakeholders, and structuring research programs. French public funding for research and development in the field of photovoltaics amounted to 78 million euros in 2023 (latest available data) out of a total of 183 million euros for all renewable energies.

The Photovoltaic Institute of Île-de-France (IPVF) and the National Institute for Solar Energy (INES) are two other major institutions involved in photovoltaic research in France. The former focuses on upstream research and advanced photovoltaic technologies, while the latter is more oriented towards applied research and demonstration projects. However, both organizations collaborate with companies to validate the technological advances resulting from their research in the marketplace. In collaboration with the manufacturer Voltec Solar, the IPVF is notably participating in the STaFF (Industrial Sovereignty Tandem of French Manufacturing) project, which aims at accelerating the industrialization of perovskite/silicon tandem photovoltaic modules. INES is working on low-carbon modules and improving the efficiency of perovskite/silicon tandem cells (up to 30.8% by January 2025) and heterojunction silicon cells. Recently, new research areas have been added, such as accelerated degradation testing to better understand cell aging, and the recycling of end-of-life panels, including module delamination and the recovery of materials such as silver, copper, and silicon.

The principal state agencies that are financing research are:

- the National Research Agency (ANR), which finances projects through topic-specific or generic calls and also through tax credits for internal company research.

- The French Agency for Ecological Transition (ADEME), which runs its own calls for R&D on renewable energies and supports PhD students. It is the French relay for the IEA PVPS and M-ERA.net pan-European network.

Industry and Market Development

While annual volumes of new connections previously rarely exceeded one gigawatt, the growth of the French solar photovoltaic sector took on a new dimension in 2022.

The connected capacities reached 2.8 GWDC in 2022, 4.0 GWDC in 2023, 6.0 GWDC in 2024, and preliminary figures for 2025 indicate an addition of 7.6 GWDC—a record for the country. Thanks to that, France’s total photovoltaic capacity peaked at 38.3 GWDC by the end of 2025, with nearly 1 135 million installations. Solar technology has thus become the leading national renewable electricity sector in terms of installed capacity, ahead of hydropower (26 GW). In addition to installed capacity, the list of projects that have obtained all necessary permits and are awaiting grid connection reached 45 GWDC by the end of 2025 (36.9 GWAC, a stable level compared to 2024).

However, despite these very high figures, the growth of activity in the photovoltaic market in 2025 was slowed by a change in the regulatory framework that took effect in March of the same year. The months-long time lag between sales and grid connections explains why growth in new capacity was largely unaffected, except in the residential segment. In 2025, large-scale roof-mounted systems and solar parking canopies ranging from 100 to 500 kWp constituted the leading segment, accounting for 44% of the additional capacity installed and 3.3 GWDC (+50% compared to 2024). With 2.5 GWDC (+23% compared to 2024), large ground-mounted plants and roof-mounted installations also remain a pillar of the development of the French solar sector, accounting for 33% of the capacity added in 2025. In contrast, the growth in newly connected capacity for residential systems (up to 9 kWp) slowed significantly, to 0.9 GWDC (-25%). 4.8 GWDC of capacity was called in 2025, with 4.0 GWDC awarded under the Contracts for Difference (CfD) organised by the French Energy Regulator, CRE, (compared to 2.9 GWDC put out to tender / 2.7 GWDC awarded in 2024). Given a delay of 2 to 3 years between the announcement of the winning bids and their connection to the grid, an additional 4 GWDC of capacity can be expected to be connected in 2026 and 2027 for large-scale installations.

Furthermore, the growth of self-consumption remains very strong in France. According to the most important French DSO, Enedis, the number of domestic self-consumption installations increased by 39% in 2025 to reach 484 734 plants, representing an installed capacity of 6.5 GWDC. The fact that the total sale of electricity is no longer possible for residential installations since March 2025 has further strengthened self-consumption trend. Collective self-consumption is also continuing to grow. Since collective self-consumption was legally introduced in 2016, the regulatory framework for this type of projects has become increasingly flexible, notably with the raise of the project cap to 5 MW (10 MW for projects led by local communities). By the end of 2025, collective self-consumption represented 1 625 operational projects with a total capacity of 0.3 GWDC.

Regarding employment and economic activity, the latest available data are for 2024. Direct full-time equivalent jobs are estimated at 37 000, a figure showing a sharp increase compared to 2023 (27 560, +34%). In terms of revenue, the sector’s activity in France is estimated at 14.65 billion euros in 2024, also showing a strong growth (+29%). However, these figures are expected to decline in 2025: several companies (particularly installers in the residential segment) have announced job cuts to adapt to the market slowdown.

Participants

Task - 1

Becquerel Institute France

Task - 12

Department of Solar Technologies (CEA-LITEN)

Claire AGRAFFEIL

Nouha GAZBOUR

Mines ParisTech

Paula PEREZ-LOPEZ

TotalEnergies

Task - 13

Institut National de l'Energie Solaire (INES), Laboratoire des systèmes Solaires (L2S)

Ioannis TSANAKAS

TotalEnergies

Dounya BARRIT

Nikola HRELJA

Task - 15

EnerBIM

Philippe ALAMY

Scientific and Technical Centre for Building (CSTB)

Laurent CALDERON

OLIVE François

Simon BODDAERT

Thierry GUIOT

Task - 16

Ecole Polytechnique à Palaiseau

Jordi BADOSA

Sylvain CROS

Electricité de France (EDF R&D)

Bruno CHARBONNIER

LLAVORI Jeanne

European Space Agency

Quentin PALETTA

Laboratoire PIMENT, University of Reunion

David MATHIEU

Philippe LAURET

Mines ParisTech

Lionel MENARD

Yehia EISSA

Yves-Marie SAINT-DRENAN

Réseau de Transport d'Électricité (RTE)

Laurent DUBUS

TotalEnergies

Arttu TUOMIRANTA

Task - 17

French Alternative Energies and Atomic Energy Commission

Bruno ROBISSON

CHAMBION Bertrand

PFEIFFER Nicolas

SAP Labs France

Jean-Christophe PAZZAGLIA

Université de Technologie de Compiègne

Manuela SECHILARIU

Task - 19

HESPUL

Vincent KRAKOWSKI

Independent Expert

Karim MEGHERBI

Lorraine University

Ayat-Allah BOURAMDANE

UPEC