2025 Country Update

{kind=link}

National PV Policy

Malaysia's energy policy supports economic growth while advancing the national energy transition and sustainability goals. The National Energy Policy 2022–2040, the Malaysia Renewable Energy Roadmap (MyRER), and National Energy Transition Roadmap (NETR) provide the main frameworks guiding this transition.

Under NETR, Malaysia aims to achieve 70% renewable energy installed capacity and carbon neutrality by 2050, with solar photovoltaic (PV) serving as a key driver. By the end of 2025, Malaysia has successfully achieved interim capacity target of 31% installed capacity dominated by hydro and PV.

The government promotes PV deployment through several schemes including Feed-in Tariff (FiT), Net Energy Metering (NEM), Large Scale Solar (LSS), and Self-Consumption (SELCO). The Energy Commission oversees the LSS and SELCO programmes, while the Sustainable Energy Development Authority (SEDA) Malaysia manages the FiT and NEM initiatives. Nonetheless, these initiatives are not executed in Sarawak due to its separate electricity supply ordinance. In Sabah, the energy sector is regulated by the Energy Commission of Sabah (ECoS).

The FiT programme established in 2011 allows the electricity generated from renewable energy (RE) sources to be sold to the grid at premium prices. Since 2016, solar PV has been phased out from the FiT programme, with support continuing only for biomass, biogas, and small hydro. In 2025, improvements were made to FiT 2.0, including revisions to the tenure and tariff structure. The Renewable Energy Power Purchase Agreement (REPPA) tenure was standardized to 21 years for biomass, biogas, and small hydro projects. Previously, the REPPA tenure was 21 years for solar PV and small hydro, but only 16 years for biomass and biogas. Additionally, FiT 2.0 implements a two-phase tariff structure, with SEDA determining the rate for the first ten years and qualifying producers bidding for the remaining 11 years.

The NEM programme, introduced in 2016, allows PV owners to offset their electricity consumption. The programme concluded in June 2025, with more than 2 600 MW of quota awarded. It will be replaced by the Solar Accelerated Transition Action Programme (Solar ATAP) starting January 2026. Solar ATAP provides greater flexibility than NEM, as it eliminates quota restrictions, provides a continuous program without a predetermined end date, and higher capacity limits for three phase domestic users (single phase ≤ 5 kWac; three phase ≤ 15 kWac) For non-domestic users, installations can reach 100% maximum demand capped at 1 000 kW. Domestic users offset their electricity consumption based on the regulated retail tariff, while non-domestic users under Solar Atap are credited at based on System Marginal Price (SMP).

In 2025, Sarawak launched its own policy framework, Sarawak Energy Transition Policy (SET-P) outlining the state’s strategy to achieve their energy transition target. Among the programmes introduced is a subsidy scheme under the NEM programme. The NEM subsidy will apply for successful NEM Installation from 2026 under the Domestic Tariff category for landed residential properties.

Following LSS PETRA 5 in 2024, the Ministry of Energy Transition and Water Transformation (PETRA) announced a supplementary round of bidding (LSS PETRA 5+) in early 2025, offering 2 GW of capacity. The programme allocates 1,500 MW for ground-mounted solar projects and 500 MW for floating solar projects, with projects targeted to be operational between 2027 and 2028. Out of the total quota, 1,975 MW was successfully awarded.

SELCO (Solar for Self-Consumption) applies when electricity generated from solar PV is used for on-site consumption only, with no export to the grid. The SELCO guidelines were revised in 2025, introducing more relaxed rules to encourage wider adoption of on-site solar, particularly among commercial and industrial users. Key changes include the removal of the 85% capacity limit for non-domestic users, allowing systems to meet up to 100% of electricity demand, and the expansion of installations to include ground-mounted and floating solar. The mandatory BESS requirement for systems above 72 kWp has been deferred until 31 December 2025, while a standby charge applies only to systems above 1 MWp (about RM12/kWp per month). The programme has also been extended to agricultural users.

On the other hand, several initiatives facilitate the virtual purchase of solar energy by consumers, including the Corporate Green Power Programme (CGPP), Corporate Renewable Energy Supply Scheme (CRESS), and Community Renewable Energy Aggregation Mechanism (CREAM). CRESS was introduced in 2024 to boost renewable energy adoption, including solar, by allowing direct electricity supply from RE developers to corporate consumers through the grid. Initially, CRESS mainly targeted new electricity demand, such as companies expanding capacity or establishing new facilities. Following a revision effective 1 March 2025, the scheme was expanded to all existing medium- and high-voltage TNB customers, allowing companies to procure renewable electricity without increasing their electricity demand. The update also streamlined the application and contracting process, making the scheme more accessible to both developers and corporate buyers. A System Access Charge (SAC) is imposed for grid usage, was revised to 25 cent/kWh for firm energy with battery storage and 45 cent/kWh for non-firm energy.

The CREAM mechanism enables residential rooftops to be aggregated for solar PV generation, allowing homeowners to lease their rooftop space to third-party developers. Based on the concept of open grid access, developers can connect multiple rooftops to form distributed solar systems that supply renewable electricity to neighbouring consumers within a 5 km radius. Participating energy firms administer rooftop leasing agreements with homeowners. CREAM projects are subject to a Community Access Charge (CAC) of 15 cent/kWh for the use of the distribution network; this charge was later reduced by 40% to 9 cent/kWh, significantly improving project economics and enhancing the programme’s attractiveness. Under this mechanism, the first flagship project in City of Elmina, developed by Sime Darby Property, aim to lease 6 000 residential rooftops within a 5 km radius for PV installations to generate electricity for nearby commercial and industrial users.

To further support RE adoption, the government waived the 1.6% Renewable Energy Fund (KWTBB) charge on electricity tariffs for the Green Electricity Tariff (GET), CRESS and CREAM programmes. The exemption aims to encourage greater participation from corporate and industrial consumers while supporting the government’s goal of accelerating renewable energy development and integration into the national electricity supply.

Financial assistance, investments, incentives, and rebates are provided to promote the adoption of renewable energy and accelerate the energy transition. The Green Technology Financing Scheme (GTFS) 4.0 continues with a total allocation of RM1 billion until December 2025, supporting six sectors, including energy. Additionally, the National Energy Transition Facility (NETF) supports energy transition projects by functioning as a blended finance platform that attracts public, private, and international funding. Malaysia Debt Ventures Berhad, as one of the implementing agencies for NETF, has approved approximately RM122.65 million in financing for several projects, including those in the energy sector, along with about RM40.09 million in targeted incentives for six technology-based companies.

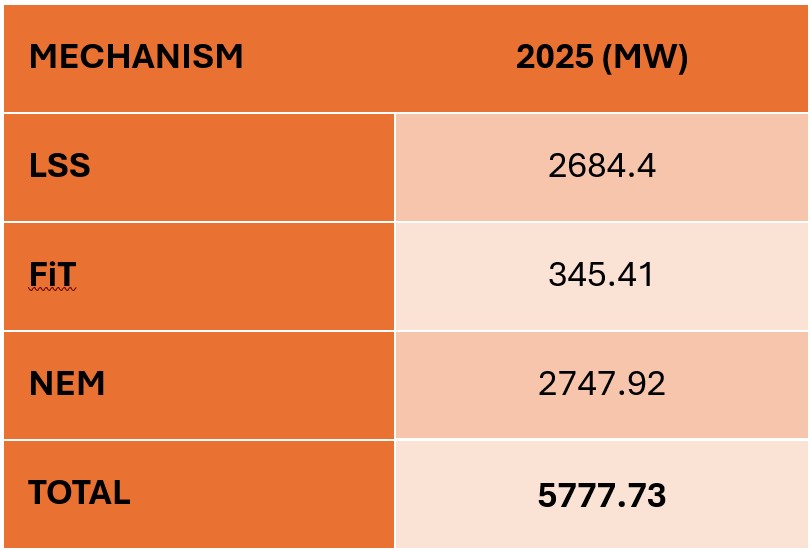

LSS Update: The LSS program has achieved 2 237 MW cumulative capacity installed capacity by the end of 2025. In 2025, a total of 60 MW of LSS capacity was commissioned, comprising two floating solar plants, DTU 1 and DTU 2, located in Pasir Mas, Kelantan.

FiT Update: As of 2025, the cumulative FiT capacity (biogas, biomass, WTE, small hydro and PV) for Peninsular Malaysia and the Federal Territory of Labuan is 1 225.29 MWac, of which 618.84 MWac is operational. Solar PV projects are fully operational and represent the largest segment of active projects, with a total capacity of 345.41 MW.

NEM Update: Since its implementation in 2016, the NEM program has provided a cumulative quota of 3 000 MWac through a series of implementations. NEM 3.0 operates across three distinct categories: NEM Rakyat, NEM GoMEn, and NOVA (Net Offsets Virtual Aggregation), with corresponding quotas of 700, 100, and 1,700 MWac. By the conclusion of 2025, 87.71 % of NEM quotas have been subscribed with a cumulative capacity of 2747.92 MW.

Research, Development and Demonstration

As of 2025, Malaysia achieved a total of cumulative capacity of 5 777.73 MW from solar PV installation under the LSS, FiT and NEM schemes.

The breakdown of the installation is shown in the following table:

Industry and Market Development

The PV industry in Malaysia has undergone significant transformation due to global trade policies, particularly U.S. tariffs and China’s export tax adjustments, as well as domestic electricity tariff restructuring.

The PV industry in Malaysia has undergone significant transformation due to global trade policies, particularly U.S. tariffs and China’s export tax adjustments, as well as domestic electricity tariff restructuring. The United States has imposed high anti-dumping and countervailing duties on solar products imported from several Southeast Asian countries, including Malaysia, increasing the cost of Malaysian exports to the U.S. market. This has contributed to weaker export demand and placed financial pressure on manufacturers operating in Malaysia. In response to these trade restrictions and broader market challenges, several PV manufacturers in Malaysia, including First Solar, Jinko Solar, Risen Energy, JA Solar, and LONGi, have scaled back operations or ceased manufacturing activities.

Despite these challenges, solar PV prices in Malaysia have remained low, largely due to oversupply from China and continued production from domestic manufacturers. Intense competition has led to a sustained price war, enabling Malaysia to procure PV systems at relatively low cost. As a result, solar PV installations have increased, supported by government incentives and rising electricity tariffs, which have improved the economic attractiveness of solar adoption.

China’s reduction of VAT export rebates for PV products (wafers, cells, and modules) from 13% to 9% in December 2024 has increased export costs and placed upward pressure on global module prices, including in Malaysia. However, due to persistent oversupply and intense price competition, the impact was muted throughout 2025, with prices remaining low until gradual increases emerged toward the end of the year. Higher solar module prices are expected in 2026 following the full removal of VAT export rebates.

In parallel, Malaysia’s electricity tariffs, typically reviewed every three years, have recently been revised upward, reflecting higher generation costs driven by rising fuel prices and increased investment in grid infrastructure. The tariff adjustment announced in the third quarter of 2025 does not affect approximately 85% of domestic users but poses challenges for industrial consumers. In response, the government has introduced measures to improve energy efficiency and mitigate cost impacts, including the Energy Efficiency Incentive, Time-of-Use (TOU) scheme, targeted subsidies, and the Automatic Fuel Adjustment (AFA), which replaces the Imbalance Cost Pass-Through (ICPT) mechanism. The TOU scheme promotes more efficient electricity consumption by charging higher rates during peak periods and lower rates during off-peak hours. Overall, rising electricity tariffs are expected to further support RE adoption, particularly solar, while encouraging more efficient energy use.

Meanwhile, grid flexibility and stability are essential for managing the variability of RE sources. Energy storage systems play a critical role by storing excess electricity generated during periods of high solar production and releasing it when demand increases, thereby improving overall grid stability. Energy Commission recently announced successful bidders for grid-connected Battery Energy Storage System (BESS) projects under the MyBEST programme, with a total capacity of 400 MW / 1,600 MWh, expected to be commissioned in 2027. Sabah has taken a major step by launching Malaysia’s first large-scale BESS project in Lahad Datu, with a total capacity of 100 MW / 400 MWh. At the regional level, initiatives such as the ASEAN Power Grid (APG), supported by the Asian Development Bank (ADB) and the World Bank, aim to strengthen electricity connectivity between Southeast Asian countries. Improved regional grid interconnection can increase electricity system flexibility and facilitate higher renewable energy penetration across the region.

Participants

Task - 1

Task - 18

Sarawak Energy Berhad

Shuin CHEN

Task - 19

Tenaga Nasional Berhad