2025 Country Update

National PV Policy

The European Union has passed several directives and regulations to shape the deployment of solar PV.

The main framework is set in the European Climate Law, which requires a reduction of EU’s greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels. Additionally, the Renewable Energy Directive set a binding target for renewables to make up at least 42.5% of total energy consumption by 2030, with an indicative 45% ambition. According to the EU Commission estimates, the 42.5% binding RES target corresponds to an indicative benchmark of 69% of renewable electricity generation by the same year.

During the 2022 energy crisis, the EU Commission also published the REPowerEU plan to phase out Russian fossil fuels and accelerate the green transition. As part of it, the EU Solar Energy Strategy aims to reach 400 GWDC of cumulative solar PV capacity by 2025 and 750 GWDC by 2030 – the former target has been narrowly surpassed at the end of last year.

More specifically for rooftop solar, the Energy Performance of Buildings Directive introduced the EU Solar Standard, making solar installations progressively mandatory on new public and commercial buildings by 2026, renovated non-residential buildings by 2027, new residential buildings by 2029 and existing public buildings by 2030.

Nevertheless, over the recent years, the deployment of solar has not been limited by the demand, but by energy system framework constraints. EU grids are unable to assimilate the electricity coming during peak-production time of renewables, especially solar, leading to curtailment and a growing amount of hours with negative electricity prices, hampering the business case of solar PV.

To remedy this, the EU Commission introduced several legislative packages aiming at improving the flexibility of the EU electricity system. Among the key files, the Electricity Market Design reform requires transmission system operators (TSOs) to develop a common flexibility‑needs assessment methodology. By December 2026, Member States must publish national objectives for non‑fossil flexibility, covering both energy storage and demand response.

At the same time, the Grids Package removes major barriers for deploying flexible assets by streamlining permitting for storage, reforming grid connection rules through first ready first served queue management, and enabling flexible connection agreements. These measures create more predictable and efficient access to the grid for battery storage and demand response while embedding flexibility into both system planning and day-to-day operations.

Aside from supporting deployment, grid integration and flexibility, the Net-Zero Industry Act (NZIA) was passed in 2024 to strengthen Europe’s clean‑tech manufacturing, including solar PV. The NZIA aims to build a more resilient value chain and reduce dependence on imports for strategic clean-tech technologies, including solar components and batteries. Member States are required to introduce resilience, environmental and other non-price criteria in auctions, public procurement, and other forms of public support, starting from 2026. The legislation aims for the EU to produce at least 40% of its demand in clean-tech technologies by 2030.

Research, Development and Demonstration

Solar PV is set to become the main source of electricity in Europe, supported by rapid cost declines, large deployment targets and the electrification of transport, heating and industry.

Current EU work on research and development therefore focuses on ensuring that solar can be integrated securely and efficiently into the energy system, supported by digitalisation, storage, flexible grids and updated market rules. These efforts align with broader goals such as energy security, competitiveness and reduced dependence on fossil fuel imports.

European R&D also prioritises next-generation PV technologies. Key focus areas include perovskites, tandem cells, advanced silicon concepts and improved manufacturing processes. Work is ongoing to enhance stability, scalability, lifetime, and the removal of critical materials, along with the development of new inverter technologies capable of grid-forming operation, higher voltages and improved digital monitoring. These efforts support the EU ambition to strengthen its industrial base and remain competitive in a fast evolving global PV market.

Innovation is expanding PV use into new applications. Significant work is underway on building integrated PV, vehicle integrated PV, Agri-PV and floating PV, each requiring specific design, durability, and permitting solutions. Research is developing digital twins for Agri-PV, optimised floater structures for offshore systems and high-voltage architectures for industrial electrification. These activities aim to unlock new deployment areas, reduce system constraints and ensure that PV can serve diverse sectors across Europe.

Sustainability and circularity form another major priority. Europe is investing heavily in repairability and reuse, material recovery, recycling processes, and unified environmental and social life-cycle assessment methods. Improving module lifetimes, reducing the carbon footprint, expanding reuse, and ensuring reliable long-term performance are key tasks. Additional work targets better risk mitigation, predictive maintenance and improved diagnostics for residential systems. These initiatives aim to ensure that solar expansion in the EU is environmentally responsible, resource efficient and supported by EU citizens.

Industry and Market Development

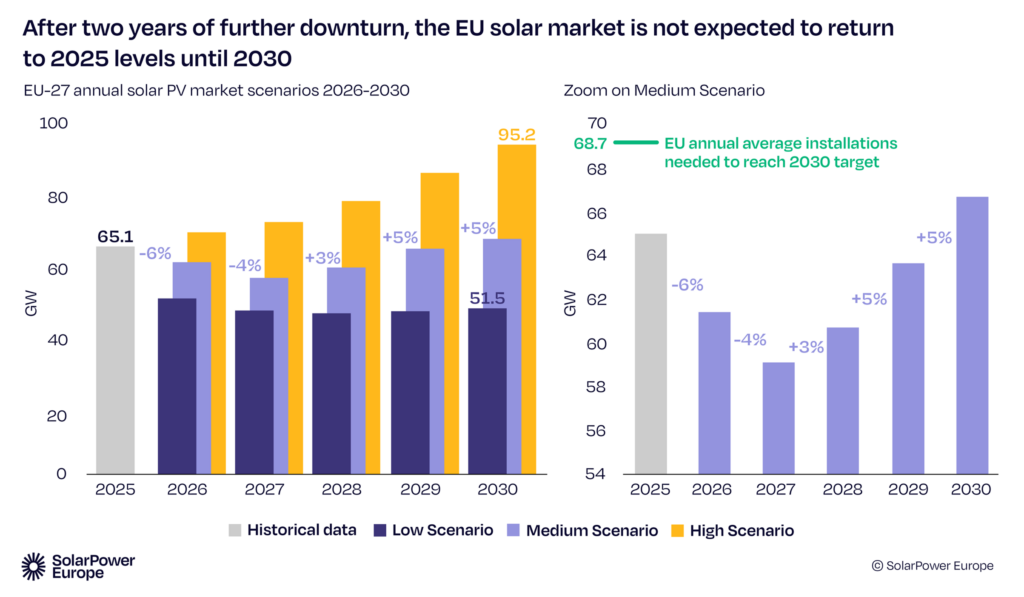

After a decade of high expansion, the EU solar market declined slightly in 2025, installing 65.1 GW, compared to 65.6 GW in 2024, marking a 0.7% decrease.

The slowdown reflects the fading impact of the energy crisis that had previously accelerated rooftop deployment. Before the recent conflict escalation in the Middle East, gas and electricity prices had remained at high levels, but the sense of urgency for households and businesses to invest in solar had diminished compared to the previous years. At present, current geopolitical developments are difficult to read, but could lead to another wave of strong interest in self-sufficiency and energy independence.

Rooftop support schemes in several key markets have been phased out, contributing to a visible decline in the distributed segment. On the utility-scale side, auctions, corporate PPAs and earlier merchant projects continue to support activity, but grid congestion, rising negative-price occurrence and policy uncertainty weigh on solar bankability.

Nevertheless, solar PV’s contribution to the EU power system is growing quickly and represented 13.2% of the electricity generation in 2025, more than doubling its 2021 share of 5.7%. In June 2025, solar PV even became the first source of electricity in the EU, generating 22% of total power output during that month, according to SolarPower Europe’s EU Solar Market Outlook 2025-2030.

The structure of the EU solar market shifted noticeably in 2025 as rooftop activity slowed down while utility-scale installations took the lead. The residential (0-10 kW) and C&I (11-999 kW) segments, which have traditionally been the driving force of EU installations, jointly represented only 47% of new installations in 2025. Residential solar observed the steepest decline, reflecting the phase-out of support schemes in several mature markets and the limited expansion of rooftop solar beyond early-adopter households. On the contrary, utility-scale solar became the main engine of EU installations, exceeding 50% of annual capacity for the first time. Despite increasingly tougher project economics, it remained the most resilient solar segment, supported by public auctions and PPA commitments made during the strong 2022-2024 period that are now reaching completion.

Looking further, EU solar installations are expected to continue declining in 2026 and 2027 before slightly recovering toward the end of the decade. In SolarPower Europe’s most updated Medium Scenario, the EU market is expected to experience two years of further single-digit contraction, followed by a slow rebound that brings annual additions back to growth territory, though at low one-digit levels, reaching around 67 GW by 2030, recovering above 2025 installation volumes only by that year.

From a cumulative point of view, the EU solar capacity reached 407 GW at the end of 2025, slightly surpassing the EU interim solar target. Nevertheless, with the annual market size not expected to grow in the coming years, the cumulative capacity in 2030 is poised to reach 718 GW, missing the 750 GW target by about 30 GW, as per our Medium Scenario.

Flexibility is the key to further success for European solar. Without rapid deployment of battery storage, demand response, grid digitalisation and expansion, solar’s value will continue to be constrained just at a time that EU businesses and citizens are craving for affordable electricity. Negative prices and curtailment are eroding business cases, and investor confidence is weakening at a moment when Europe needs more clean energy investment for its energy security and competitiveness, and urgently needs to detach itself from volatile fossil fuel imports. For this reason, the EU needs a decisive push on flexibility with a dedicated EU Flexibility Strategy that unlocks the enormous potential of battery storage and demand-side flexibility.