2025 Country Update

National PV Policy

In 2025 the gradual phasing out the successful net metering scheme has begun and will finish in 2027. At the same time subsidy schemes for electrical vehicles and heat pumps were cancelled and in general the market has not been favorable.

New elections and a change of government in 2026 may alter these general policies. In the meanwhile the solar sector, in anticipation, has moved to integrated solar-battery products, dynamic energy contracts and revisiting solar integrated products like solar car ports, BIPV, floating PV and even combining these systems in so called energy hubs.

The major driver for these developments has been increasing grid congestion which has persuaded also companies to look for alternatives and higher levels of self-consumption with renewable energy sources and storage. Waiting lists for new grid connections have grown and new plans for solar parks are advised to look into the options with battery storage, cable pooling, peak shaving and congestion management.

In 2025 the SDE++ category for larger systems (> 15 Kwp) the available budget reached 8 billion euros but stricter condition were put in place to encourage more nature inclusive solar parks, for example with vertical solar panels.

The Netherlands remain committed to achieving net zero carbon emissions by 2050 but according to the national environment assessment agency PBL, the chances of reaching the mid-term goals of 55% emission reduction in 2030 have become extremely small.

More and more the focus is shifting towards system integration of renewable sources like solar and wind as these infrastructural and societal barriers are hit. However the lead times for grid reinforcement are long and therefore a renewed interest in decentralized systems has reemerged. A national program on energy hubs started with a modest budget for R&D. RVO estimates that over 1,000 locations are suited with another 3 GWp of capacity by 2030.

Cyber security of the energy infrastructure remains another priority and together with higher levels of resilience is shared with other ministries and exceeds the climate policies.

Research, Development and Demonstration

In 2025 the mission oriented R&D programme topics remained largely the same:

- Renewable Energy Production

- Energy Saving

- Flexibility of the Energy System

- Circular Economy

- Natural gas free Neighborhoods and Buildings

In 2025 the first independent quality label for new solar parks was published by the TNO led consortium Eco-Certified. It not only guarantees sustainable and autonomous energy production but also delivers measurable benefits for soil quality, biodiversity, and the landscape.

Higher technology readiness levels (TRL) are managed in separate programs for fundamental research by the national organizations NWO and STW. The research activities themselves are dispersed over several universities and research institutes like AMOLF, DIFFER, TNO (the national institute for applied research) and several universities.

The National Growth Fund project SOLARNL started in 2023, received strong head winds in the international market but is making piecemeal progress on specific technical topics, training and education.

Industry and Market Development

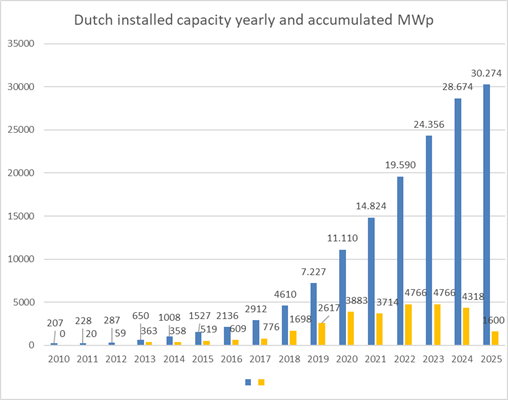

The accelerated growth of the solar PV market flattened out in 2023 and the market for solar panels stabilized in 2024 on a somewhat lower level.

For 2025 however mixed messages are surfacing using different sources. The CBS reported 647 MWp installed in the first half of the year.

Usually a similar result for the second half of the year can be assumed but this year there is a large degree of uncertainty and the figure here in table 1 is a rough first estimate based also upon preliminary data from the SDE plus scheme by RVO.

Both the solar roof top market and ground mounted systems have reached levels where the proverbial “low hanging fruit” has been plucked. Over 50% of house owners have now installed solar panels in the Netherlands while the rental home market falls behind with an estimated 20%. On business parks and utility construction there is still much space but congestion and split incentives obstruct a faster roll out. All markets are therefore changing towards more integrated products and higher degrees of self-consumption within the home, company or so called energy hubs.

Home owners are increasingly combining solar panels with home battery storage which will have to be integrated with energy management systems (EMS) and the same goes for EV’s. Heat pumps are another enabler of solar PV and its market share is on the rise but still an early adopter market.

Energy communities are on the rise but are struggling in the current market setting. In the Netherlands an update of the energy law is planned for the beginning of 2026.

Solar parks can already use battery storage and cable pooling to relieve the national grid. The national grid operator Tennet has reduced transport tariffs to a maximum of 65% for larger solar parks with battery storage and expects an increase with these measures up to 5 GW of battery capacity for flexibility.

The niche market of BIPV remains predominantly a business to business market notwithstanding government initiatives that target renovation of the existing building stock and social housing in particular.

VIPV is taking of in the market segment for trucks and semi-trailer and setting international examples.

The result is a drop in the growth of the installed capacity in the Netherlands and unforeseen effects on the solar hours produced by increasing curtailment measures.

The market may perform a little better in the second half of the year and possibly reach 1.6 GWp of newly installed capacity which is significantly lower than in years before. The total amount of installed capacity over the years will probably exceed the 30 GWp.

Participants

Task - 1

Task - 12

Delft University of Technology

Malte VOGT

Netherlands Organisation for Applied Scientific Research (TNO)

Mirjam THEELEN

SmartGreenScans

Mariska de WILD-SCHOLTEN

Task - 13

Utrecht University

Mirbagheri (Sara) GOLROODBARI

Task - 15

ZUYD

Zeger VROON

bear-ID

Tjerk REIJENGA

Task - 16

Utrecht University

Wilfried VAN SARK

Task - 17

Netherlands Organisation for Applied Scientific Research (TNO)

CARR Anna J.

Task - 18

Delft University of Technology

BAUER Pavol

RAMIREZ ELIZONDRO Laura

Task - 20

Delft University of Technology