2025 Country Update

{kind=link}

National PV Policy

The Clean Energy Superpower Mission sets out the UK’s ambition to become a global leader in clean energy by delivering Clean Power by 2030 and accelerating progress toward Net Zero.

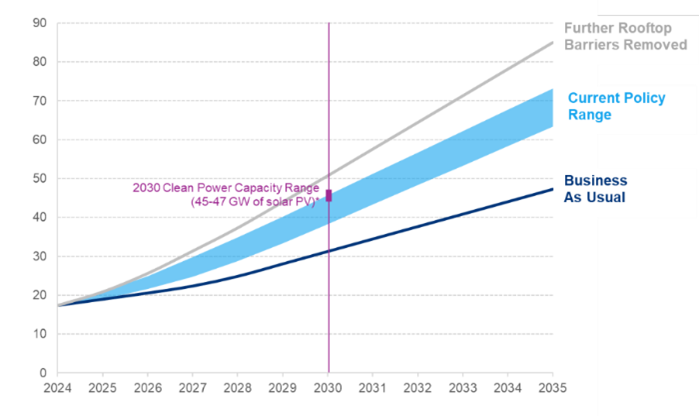

The mission focuses on four major outcomes: enhancing energy security, protecting billpayers, creating economic growth and green jobs, and reducing greenhouse gas emissions. Central to this effort is the Clean Power 2030 Action Plan, which includes commitments for clean energy to produce at least as much power as Great Britain (GB) consumes, deliver at least 95% clean generation, and reduce the carbon intensity of electricity generation to below 50 gCO2e/kWh by 2030. It also calls for the rapid acceleration of solar deployment, from over 21.6 GW at present, to 45-47 GW by 2030.

The UK’s Solar Roadmap, published in 2025, sets out a national plan to accelerate solar deployment to support its clean energy strategy, highlighting solar as one of the cheapest power sources. The Roadmap outlines 72 actions to remove barriers to solar deployment, including through the £15 billion Warm Homes Plan which will help households take up measures such as solar panels and batteries. The upcoming Future Homes Standard will also ensure solar panels are installed on most new build homes.

For the commercial and public sectors, the removal of the 1 MW planning cap simplifies rooftop deployment, while new permitted development rights will allow solar canopies in car parks. In addition, the threshold for requiring complex grid assessments has been raised from 1 MW to 5 MW in England and Wales, exempting all rooftop solar projects, lowering costs and speeding up connections.

The main mechanism for supporting large scale solar PV deployment in the UK is through the Contracts for Difference (CfD) scheme, which was launched in 2014. In the most recent allocation round, a total of 4.9 GW of solar capacity was awarded, with 1.9 GW expected to come online by 2028 and the remaining 3 GW by 2029. The Roadmap commits to targeting CfD reforms to ensure the scheme can accommodate the volume of new solar needed for Clean Power 2030 while keeping

consumer costs low, and is reviewing how innovative technologies such as floating solar are treated within the scheme. UK Companies can also access Government-backed finance through several organisations including the British Business Bank (BBB), the National Wealth Fund (NWF) and UK Export Finance (UKEF).

The Roadmap further outlines actions to address barriers relating to planning, grid connections, supply chain and skills, while enabling innovation and alternative deployments options such as advanced solar cell technologies, plug-in solar, floating solar and space based solar power. For example, the Government has commissioned a plug-in solar safety study to explore how they can be deployed safely in the UK.

Research, Development and Demonstration

Solar technology is one of the research areas funded by the UK Engineering and Physical Sciences Research Council (EPSRC), with an estimated £37.6 million in grant funding awarded.

The scope includes:

- Fundamental materials research into new and novel materials for solar PV

- Thin-films, flexible PV and the utilisation of new materials for increased efficiency, better stability and lower costs

- Solar fuels, solar thermal and floating solar

- Systems integration

The £1 billion Net Zero Innovation Portfolio (NZIP) provided funding from 2021-25 for low carbon technologies and systems, including projects relevant to solar deployment and integration. Some highlights include:

- Open Climate Fix, funded through the AI for Decarbonisation Innovation Programme, has integrated satellite imagery, weather data and real‑time solar PV generation data to create an open‑source foundational model for forecasting near‑term, hyper‑local solar PV generation. This is now fully operational in Great Britain’s National Energy System Operator’s (NESO’s) control room, saving 300,000 tonnes of CO2 and £30 million per year in balancing costs, with potential to reach £150 million by 2035.

- Sunsave Group Ltd, funded through the Green Home Finance Accelarator, piloted a novel ‘Solar as a Service‘ model for residential rooftop solar. The Sunsave Plus solar subscription, trialled with 110 customers, provided a solar PV and battery system installation at no upfront cost, with households paying a fixed monthly subscription fee.

- The £5.5 million Space Based Solar Power Programme was launched to explore the feasibility and commercial potential of SBSP. Funding was awarded to eight leading universities and technology firms across four themes: wireless power transmission, concentrated solar photovoltaics, systems energy engineering, and space mission architecture.

Industry and Market Development

Renewables generated an average of 63% of GB’s electricity during 2025. Solar continues to grow rapidly as part of the electricity mix, accounting for roughly 6.5% of generation, an increase from 5% in 2024.

Solar PV Cumulative Installed Capacity

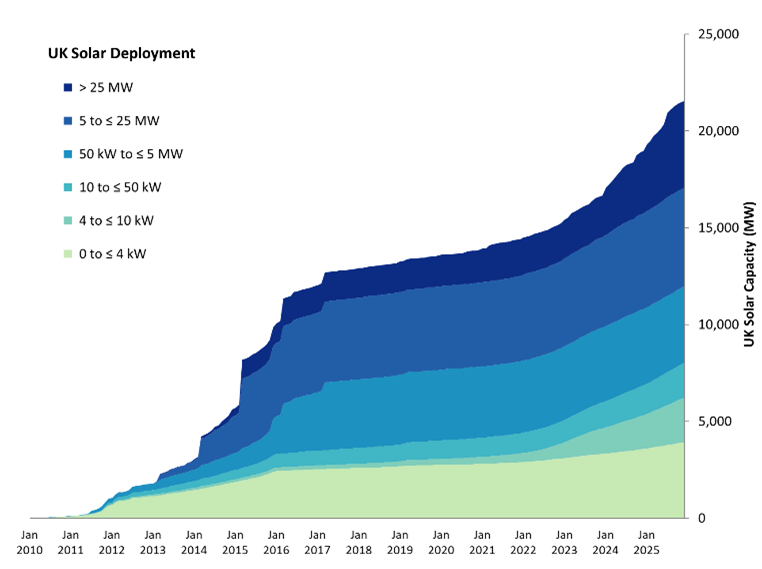

Solar reached a new maximum generation record of 14 GW on 8 July 2025. By the end of December 2025, the UK had 21.6 GW of installed solar capacity across 1 918 000 installations —an increase of 13.6% (2.6 GW) since December 2024. This includes the 373 MW Cleve Hill solar farm, which is now the UK’s largest operational solar farm.

Over the course of 2025, a total of 262 000 installations came online, the highest annual total to date. The 2.6 GW new capacity added in 2025 was the highest annual figure since 2015, when 4.3 GW was added and just behind 2014 when 2.7 GW was added.

Most solar PV installations in the UK are domestic but they only account for 29% of the total capacity. At least 40% (8.6 GW) came from ground-mounted or standalone solar installations, including 21 on CfD, 19 of which came online during 2025.

Figure 3: UK solar deployment (MW) scenarios 2010-2025.After a sharp drop in April 2020 due to Covid-19 restrictions, the number of installations recovered in late 2020 and gradually exceeded pre-pandemic levels. Between 2016 and 2021, the median monthly installations was around 3,000 per month. The median over the past 12 months was over 22,000 installations per month.

Cost Trend

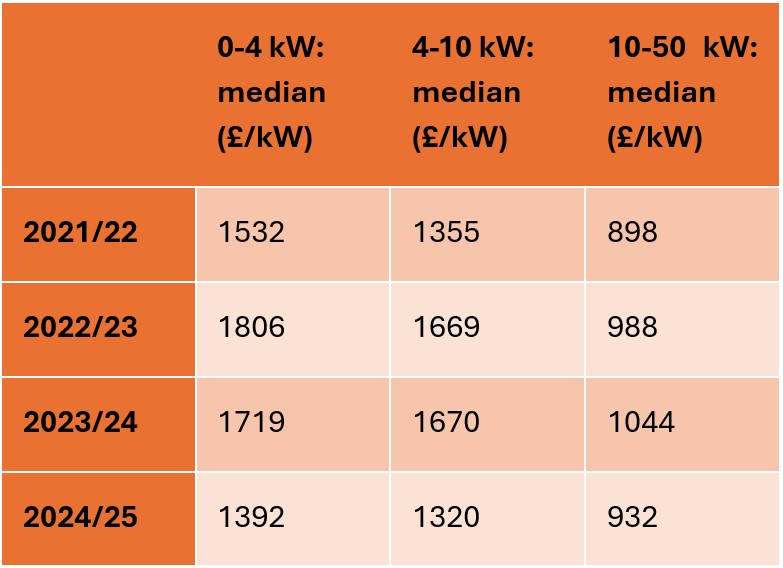

Small-scale installation costs have fluctuated, peaking in 2022/23 when median prices exceeded £2,000/kW. This was driven by a number of factors, including supply chain pressures, higher shipping costs, and increased demand pushed by high electricity prices. Prices then fell through 2024/25 to their lowest levels in years. Over the past year, median £/kW decreased for all installation sizes: by 19% for 0–4 kW, 21% for 4–10 kW, and 11% for 10–50 kW compared to 2023/24. Larger installations continue to show lower £/kW, and advances in technology alongside increased supply have driven prices down despite rising demand.

For grid scale solar, the UK’s CfD scheme provides the best indicator of cost trend. In this scheme, developers compete in an auction for long-term contracts that guarantee a fixed price for the electricity they will generate with the strike price representing the minimum revenue needed for economic viability.

Solar projects were originally allowed to compete in the first auction but were excluded in subsequent rounds. Solar was then allowed to bid again for the allocation round 4 (2022) where 3.1 GW capacity was secured. Across the years, the price of solar projects has remained the lowest of all renewable technologies. In 2024-adjusted prices, strike prices were £64.09/MWh in 2022, £65.49/MWh in 2023, and £69.77/MWh in 2024. The most recent auction saw solar strike price fall again to £65.23/MWh, representing a 10% decrease from 2024. However, this round offers 20-year contract, unlike the 15-year contracts used in all previous rounds, therefore the lower price possibly reflects longer revenue support rather than a real cost reduction.

Participants

Task - 12

Northumbria University

Neil BEATTIE

Oxford Brookes University

Marco RAUGEI

Task - 16

Peak Designs Ltd

John WOOD

Task - 19

UK Power Networks